Following the Move: Managing My Gold Put Ahead of Central Banks

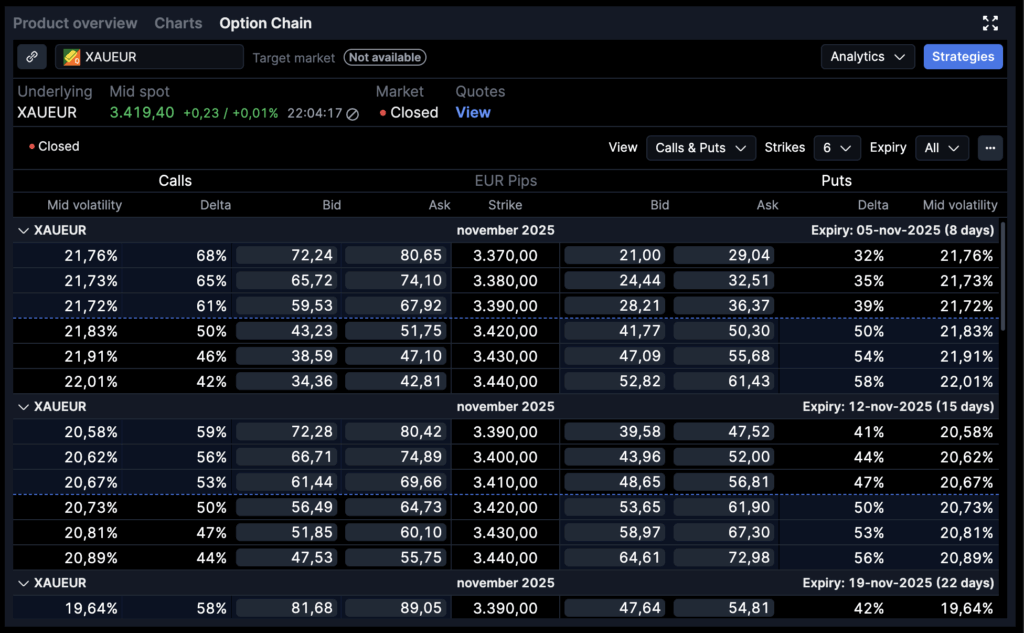

A little over a week ago, I wrote about taking a position in a 3,600 XAU/EUR put — built on a simple thesis: gold had run too far, too fast, while volatility wasn’t properly reflecting the asymmetric downside risk.

That call has played out almost perfectly so far. Gold has now broken decisively below 3,450, and intraday even tested the 3,425 zone. Implied volatility has firmed, and what began as a patient short-vol setup has turned into a clean convex trade.

The thesis remains intact. My short-term roadmap points toward 3,275 as a likely test level within the next 9 days — especially with both the FED and ECB meetings this week likely to inject renewed two-way volatility. For now, I’ve trimmed part of the position to lock in gains, keeping the rest open to capture any acceleration toward that target.

From Patience to Payoff

When I opened the trade, the logic was simple: pay a small fixed premium and let time and pressure build until the market breaks. Back then, gold was trading near 3,620 EUR/oz, volatility was subdued, and sentiment leaned comfortably bullish. Few saw room for a meaningful pullback.

Now, with spot around 3,425, that calm has cracked. The put that once seemed like quiet insurance has more than doubled in value. It’s a reminder that staying long convexity often feels uncomfortable right up until it doesn’t.

The move reinforces a lesson I keep learning in different ways: options don’t reward constant activity — they reward conviction held through boredom and disbelief. The hardest part of trading them is often doing nothing until the moment it finally matters.

The Current Setup

With just over a week left until expiry, the position sits comfortably in the money. Time decay isn’t the problem anymore — direction is. At this stage, it’s not about waiting for the clock, but about managing the movement.

If gold stalls around 3,425 or rebounds toward 3,475, the option’s value will fade quickly as volatility contracts after the central bank meetings. But if momentum extends toward my next target near 3,275, the trade could still deliver another leg higher, turning a solid gain into roughly a 2.5–3× return on premium.

That’s the kind of asymmetry worth holding on to — where risk is already paid for, and the only question left is whether the market gives one more wave before the calendar runs out.

Managing the Position

Here’s how I’m approaching it now:

If gold consolidates between 3,400 and 3,450 into the central bank meetings, I’ll hold the position as is. The expected uptick in volatility ahead of the FED and ECB should help support pricing, even if spot drifts sideways.

If momentum resumes and price moves quickly toward 3,325 or below, I’ll start taking profit in stages — first by trimming part of the position around 220 EUR, then considering a roll down to the 3,400 strike only if the move accelerates toward 3,300. It’s a balance — roll too early and you lose convexity, wait too long and the next strike gets expensive as volatility and intrinsic value build.Waiting for confirmation avoids paying up for a new option while volatility is still inflated.

If gold rallies back above 3,475 after the rate decisions, I’ll exit cleanly. At that point, the structure has done what it was meant to do — catch a directional move and monetise the convexity — and there’s no point in fighting reversion.

For me, this phase isn’t about guessing the next move; it’s about managing risk, keeping edge, and letting the trade end on my terms, not the market’s.

Looking Ahead

Technically, gold still looks fragile. The clean break below 3,500 EUR shifted the structure from consolidation to continuation, and so far, every rebound toward 3,450 has been met with selling. Unless we see a clear macro shift — something like renewed central bank demand, a dovish surprise from the FED, or a sharp euro recovery — the path of least resistance remains lower.

My working target stays around 3,275. That’s where both the medium-term support and the next cluster of option interest line up. I don’t need to predict every intraday swing; I just need the downside pressure to persist long enough for volatility to keep doing the heavy lifting.

Reflection

This trade has reinforced what I’ve always believed about options: they’re not about prediction, they’re about positioning. The edge doesn’t come from guessing where the market goes next, but from structuring exposure so that when it moves, it matters.

The goal isn’t to be right on every trade — it’s to stay positioned for the rare alignments of timing, direction, and volatility. Those moments don’t come often, but when they do, they pay for all the quiet stretches in between.

Right now, gold still feels like one of those moments — fragile, reactive, and full of potential energy. My job is simply to stay disciplined enough to let the structure do what it was built to do.