Waiting for the Next Break — Positioning After the Gold Put Exit

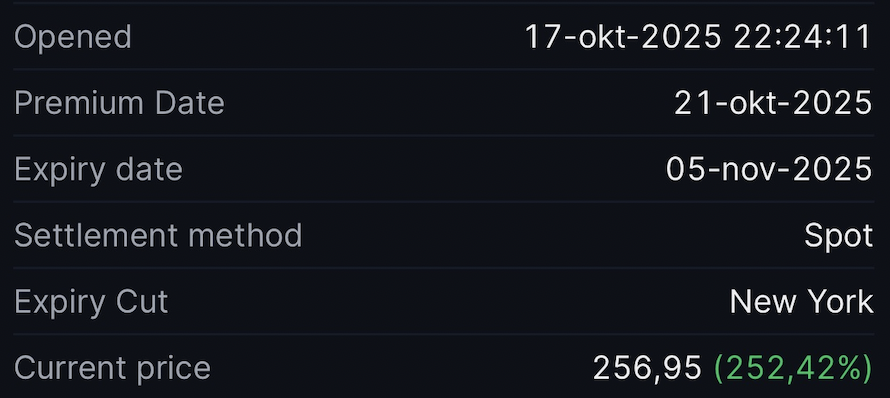

Last week, I closed out my 3,600 XAU/EUR put — a position that had evolved from quiet insurance into a sharp convex trade.

The exit wasn’t about doubt. It was about discipline. After a clean move from 3,620 to below 3,400, the trade had done what it was designed to do: capture a directional break and monetize volatility before theta turned against me.

The position delivered roughly a 250% return. Not because I guessed the future, but because I stayed long convexity until the market ran out of patience.

Now, with the slate clean and gold trading around 3,450 EUR, the question isn’t what happens next — it’s when to act again.

The Setup: Between Policy and Politics

We’re entering one of those tight macro windows where policy meets geopolitics.

- The Fed will hold rates this week, but Powell’s tone will matter more than the decision. Any hint of “higher for longer” could push the dollar higher and weigh on gold.

- The ECB follows right after, likely dovish given weak European data — a mix that could keep EUR under pressure versus USD, and leave XAU/EUR caught between competing flows.

- And tomorrow, the Trump–Xi meeting adds another layer — a wildcard that could swing sentiment violently in either direction.

For gold, the market already leans toward optimism. That means the upside in price is capped, but the real opportunity may lie in the reaction — not the event.

The Volatility Playbook

If tomorrow’s headlines are upbeat — a handshake, vague commitments, talk of “progress” — traders will rush back into risk assets.

That’s when volatility usually collapses: option premiums drop 30–40%, even as gold softens further.

That’s the window I’m watching.

- If gold bounces modestly toward 3,470–3,490 on “trade optimism”, I’ll look to buy a short-dated 3,350–3,375 put (≈19 days out).

- The move higher resets volatility.

- The skew cheapens.

- And the asymmetry returns.

- If gold drops straight through 3,350 after the meeting, I’ll wait. The next entry comes only after a retrace, when complacency sets back in.

This isn’t about chasing delta — it’s about buying optional time when the crowd stops paying attention to it.

Timing and Convexity

The key right now is patience.

Volatility will likely compress immediately after the Trump–Xi meeting and the dual central bank announcements — a rare setup where theta risk briefly disappears, replaced by optionality mispricing.

The ideal moment to act isn’t before the headlines. It’s after, when traders exhale and volatility gets mispriced downward. That’s when convexity becomes cheap again.

Forward Strategy

My forward map looks like this:

| Scenario | Market reaction | Planned action |

|---|---|---|

| Optimistic trade outcome | Gold dips, vol collapses | Buy short-dated OTM put (3,350–3,375) — low premium, high convexity |

| Neutral outcome | Brief rally in gold, muted vol | Wait for market to settle, then re-enter if rebound stalls |

| Negative or failed talks | Gold spikes short-term | Wait for vol to compress again before re-entering; no rush |

The Takeaway

The last trade rewarded patience.

The next one will reward timing.

Gold’s macro structure remains fragile — caught between fading inflation hedges and shifting political narratives.

The edge now lies not in prediction, but in waiting for the crowd to relax, then quietly buying exposure to what they’ve already priced out.

If the Trump–Xi optimism fades faster than it forms — and history suggests it often does — there will be one more chance to ride the wave.

The Geopolitical Wildcard

Beyond the trade headlines, there’s also the growing speculation around a potential Trump–Putin meeting, reportedly facilitated by Hungary.

If that happens — or even if markets start pricing it in — it could reinforce the current “risk-on” narrative, pressuring gold further as geopolitical tension temporarily eases.

But this kind of détente rarely lasts. Historically, such summits tend to deliver symbolic optimism first, then renewed uncertainty once it becomes clear that deep structural issues remain unresolved.

That’s why I see any near-term optimism as a shorting opportunity rather than a reason to chase gold higher.

Considering the Other Side: Optionality Cuts Both Ways

While my bias remains bearish in the short term, it’s worth acknowledging that volatility works both ways.

Markets often overshoot, and once positioning becomes one-sided — as it is now in gold — even a small surprise can trigger a violent reversal.

If the Trump–Xi meeting ends with little substance, or if talks between Trump and Putin reignite geopolitical tension instead of easing it, gold could catch a sharp relief bid.

In that case, a cheap, short-dated out-of-the-money call (e.g. 3,500–3,520 strike) could act as a low-cost hedge — essentially buying volatility, not direction.

That’s not a directional play, but a reversal insurance:

- Small premium outlay (theta-light, limited loss).

- Potential for an outsized payoff if volatility spikes again.

- Keeps portfolio exposure balanced if risk sentiment flips faster than expected.

I’m not planning to flip long gold outright — but as someone who trades convexity, I’d rather own optionality than opinions.